Climate hits the field while Tariffs raise the price.

TL;DR

US domestic climate shocks resulted in a 95-100% orchard loss in Utah, $150-200m of damages to specialty crops in Pennsylvania, while persistent High Plains drought continues to hit wheat. These are compounding with import-side tariffs to push US food prices higher than either pressure alone would. With the United States–Mexico–Canada Agreement (USMCA) renegotiation opening on 1 July, six weeks of policy uncertainty sit on top of the cost of US fresh produce.

This week’s top briefs

Utah declares state of emergency: 95-100% orchard losses across ten counties

Summary: On May 15th, Utah Governor Spencer Cox signed Executive Order 2026-01 declaring a 30-day state of emergency for Box Elder, Cache, Davis, Iron, Juab, Millard, Piute, Sanpete, Utah and Weber counties. Freezing temperatures on April 3, 4, 17 and 18 – recorded below 26°F for more than eight hours – destroyed an entire season's harvest of apricots, sweet and tart cherries, plums, peaches, pears and apples. An early warm spell pulled bloom three to four weeks ahead of schedule, then a routine spring cold snap landed on flowers.

Key data: Statewide fruit loss estimated at 95-100% across all major tree crops. Kent Pyne (Pyne Farms, Santaquin, fourth generation since 1903): “The trees thought, ‘Hey, winter’s over, let’s bloom,’ and so we had a bloom that was three to four weeks early, then we lost all of our fruit.” Last comparable event was in 1972. The same pattern landed in Pennsylvania (April 21 freeze, $150-200m specialty-crop losses, all-counties USDA disaster designation requested by Governor Shapiro on 8 May) and in Colorado’s North Fork Valley (entire crop destroyed).

Why it matters: Specialty fruit prices feed directly into retail CPI, and national losses leave few alternative sourcing options. Replanting is multi-year.

Read: Utah Governor’s Office — Executive Order 2026-01 · KSL News (Pyne Farms) · The Watchers — PA disaster request

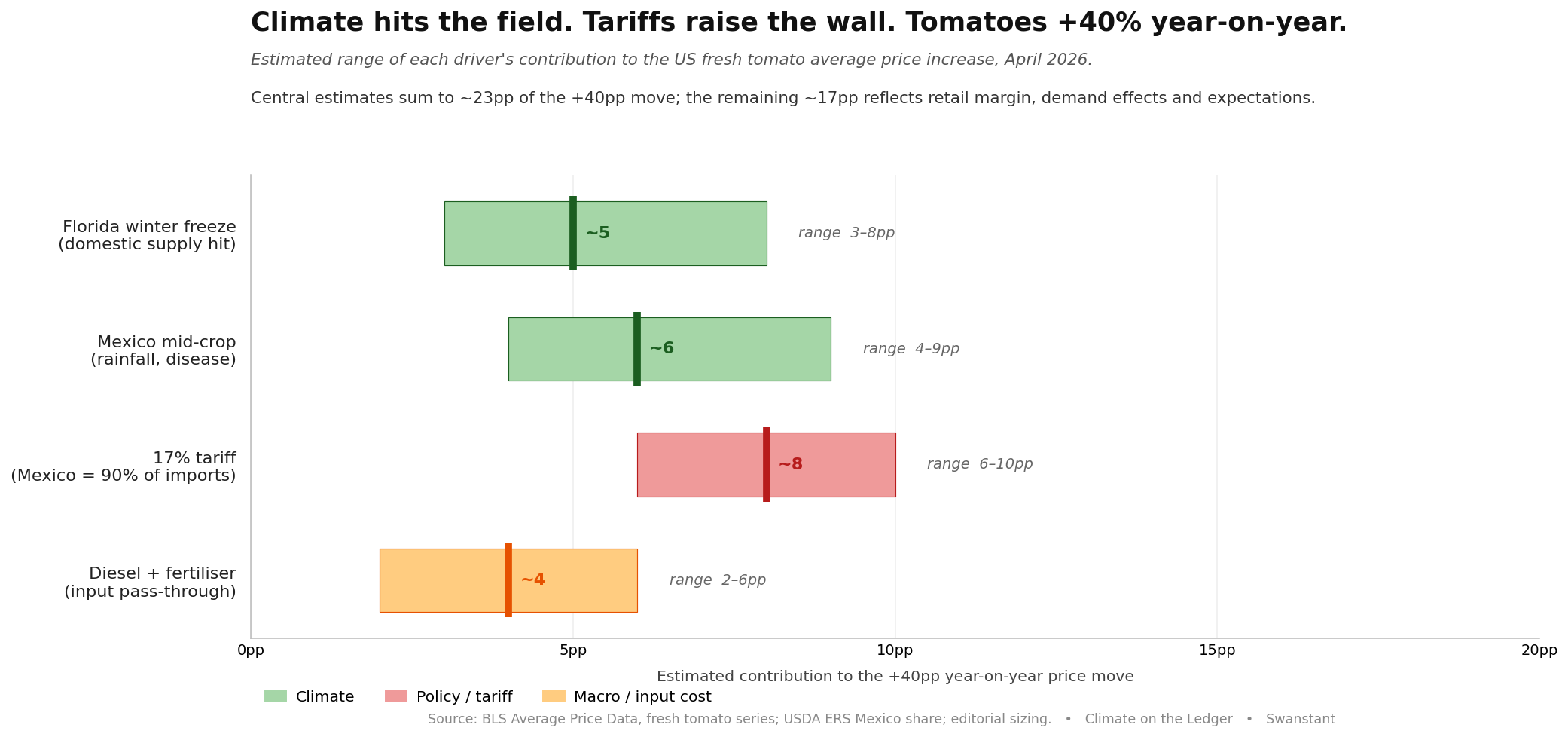

US fresh tomatoes: +40% YoY

Summary: US fresh tomato prices hit the highest April Bureau of Labour Statistics (BLS) print on record at +40% year-on-year. The move is a textbook example of the compounding thesis we defined in our recent Curb Your Sustainability analysis: Florida winter freezes cut domestic supply (hundreds of millions in damages, disaster declarations); Mexico's mid-crop yields fell on excessive rainfall and disease; the 17% tariff imposed in July 2025 – after the Tomato Suspension Agreement was terminated by Commerce – landed on top; and diesel and fertiliser costs pushed input prices higher.

Key data: BLS fresh tomato CPI +40% YoY, highest April on record. Mexico supplies 69% of US fresh vegetable imports by value and 90% of US tomato (USDA ERS, 2023; ProducePay, 2024). Tariffs on Mexico fresh vegetables at 17%. Diesel was +63% over the six months to early May before easing on Iran-talk progress.

Why it matters: Tomatoes show climate, trade and input costs hitting one crop at the same time. The same structure applies to bell peppers, cucumbers, blueberries, raspberries, strawberries and asparagus.

Read: USDA ERS — Mexican share of US horticultural imports · FreshPlaza on USDA fresh produce import shares

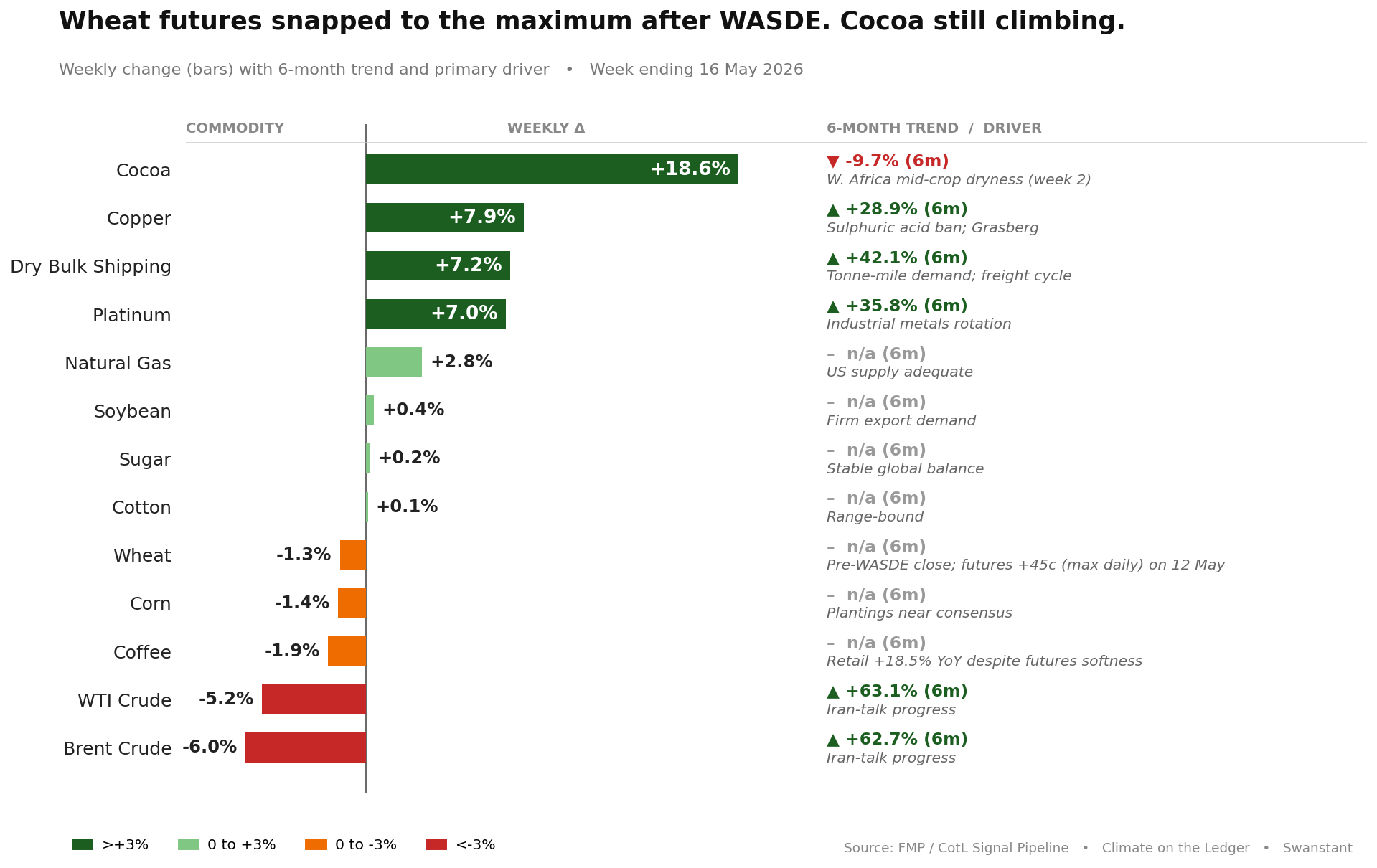

Smallest US wheat crop since 1972

Summary: The 12 May World Agricultural Supply and Demand Estimates (WASDE) delivered the first survey-based 2026/27 estimates and shocked the market. USDA projects total US wheat production at 1.561 billion bushels (bu), down 424 million on 2025/26 (−21%) and the smallest US wheat crop since 1972. Hard Red Winter production was cut 36%. Both Kansas City and Chicago July wheat futures closed up 45 cents on the day; MIAX Minneapolis ended +37½ cents. The pre-report consensus had been 1.735bn bu, and the USDA reading came in 174m below it.

Key data: 2026/27 all-wheat yield projected at 47.5 bu/acre, 5.8 bu below last year's record. Winter wheat production down 25% year-on-year to 1.048bn bu. Season-average farm price raised $1.50 to $6.50/bu. 2026/27 ending stocks projected at 762m bu, down 18% on the year. All-wheat planted area at 43.775m acres, the lowest in US history. Global wheat production cut to 819.1m tonnes from last year's record 843.8m tonnes, with reductions across the US, EU, Argentina and Australia. StoneX's Arlan Suderman notes the May 1 cut-off date means further reductions are likely as deterioration continues.

Why it matters: Wheat futures are now catching up to what's been happening in the field: Kansas City and Chicago hit the maximum daily move the exchange allows on the WASDE day. The macro picture is harder still: all six major exporters cut output outlook at once (US, EU, Argentina, Australia, Canada, Russia/Ukraine combined cut of 32.28m tonnes).

Read: USDA WASDE-671 May 2026 · DTN Progressive Farmer — Bullish Wheat Estimates Send Futures Limit Up · DTN Progressive Farmer — 2026 US Wheat Production Expected to Be Lowest Since 1972 · High Plains Journal

America’s CEOs testify on food inflation: beef, coffee, tomatoes

Summary: Reporting via Yahoo Finance compiles earnings-call commentary from US CEOs flagging beef, coffee and tomatoes as the inflation problem children. IndexBox confirms beef at $6.90/lb and coffee retail prices +18.5% year-on-year. The signal worth watching is the breadth: when food CPI moves across categories at the same time, the macro story becomes harder to dismiss.

Key data: Beef $6.90/lb (IndexBox, May 2026). Coffee retail +18.5% year-on-year despite Arabica futures down 1.9% on the week and 39.1% below the 52-week high. Tomatoes +40% year-on-year. All three are taking a mix of climate (Brazil/Colombia coffee weather, Florida/Mexico tomatoes, cattle herd drought response) and policy (tomato tariff, Mexican cattle redirected to domestic feedlots per USDA Mexico Livestock and Products Feb 2026).

Why it matters: The retail-versus-futures gap on coffee is the same disconnect we tracked on wheat for three weeks before this week's WASDE closed it suddenly. Where retail is moving faster than futures, procurement contracts indexed to futures leave the inflation on the buyer's side.

Read: Yahoo Finance via Google News (CEOs on beef, coffee, tomatoes) · IndexBox via Google News

United States–Mexico–Canada Agreement (USMCA) renegotiation opens in six weeks

Summary: The formal USMCA review begins 1 July 2026. The first bilateral US-Mexico talks started on 16 March. The Trump administration has publicly floated everything from renegotiation to splitting USMCA into bilateral deals with Mexico and Canada to letting the agreement expire. Forty US agricultural organisations launched the "Agricultural Coalition for USMCA" in February in defence of the framework. The Tomato Suspension Agreement termination in July 2025 was the precedent for unilateral US tariff action on Mexican agricultural products.

Key data: The US exports around $58bn/year of agricultural products to Canada and Mexico – approximately one-third of its agricultural export value. US exports to those markets grew 47% since USMCA took effect in 2020, versus 18% to the rest of the world. Mexico represents 51% of US fresh fruit imports and 69% of fresh vegetable imports by value. The 1944 US-Mexico Water Treaty is also being raised in the negotiations, linking water rights to agricultural trade.

Why it matters: Six weeks of policy uncertainty hangs over the half of US fresh produce that comes from Mexico, at exactly the moment climate shocks are tightening domestic supply.

Read: CSIS — USMCA Review 2026 · Baker Institute — Strategic Priorities for the 2026 USMCA Review · CBC News — Agricultural Coalition for USMCA

Adaptation Best Practice

Talbott Farms, Palisade Colorado: wind machines, water and the "Million Dollar Breeze"

Hazard: late-spring freezes on advanced-bloom orchards in the Grand Valley.

What they did: the Talbott family has built out a multi-decade frost protection stack: wind machines positioned to use the natural down-valley canyon breeze (Palisade's "Million Dollar Breeze"), sprinkler irrigation that creates a protective ice layer at 32°F, propane Frost Busters, and orchard-row campfires for the deepest cold events. Charlie Talbott reportedly spends the coldest nights "glued to his phone or racing around in a pickup truck and revving engines."

Outcome: facing the same April 18 freeze that took 95-100% of the crop at Pyne Farms in Utah and wiped out the North Fork Valley orchards near Paonia and Hotchkiss, Palisade saved an estimated 80-90% of its peach crop. Sanders Family Orchards reports just 10% loss.

Why this matters operationally: the gap between Pyne (no infrastructure, 100% loss) and Talbott (full stack, 80-90% saved) makes the case for adaptation investment in a single comparison. The cost of the infrastructure shows its return in any year where it prevents complete crop failure.

Source: The Colorado Sun on Talbott Farms · Colorado Fresh Fruit Co. 2026 updates · Scofield Fruits on Palisade vs North Fork

Data Snapshot

Tomatoes +40%, broken down

What it shows:

Climate components (Florida + Mexico) sit in a combined range of roughly 7–17pp, central ~11pp.

The 17% tariff alone sits in a range of 6–10pp, central ~8pp – close to the size of the two climate shocks combined.

Mexico’s share of the climate story is larger than Florida’s because Mexico supplies roughly 57% of US fresh tomato consumption versus Florida’s ~12%. Even a smaller percentage yield decline in Mexico translates to a comparable absolute price impact.

Named drivers explain somewhere between two-fifths and four-fifths of the year-on-year increase. The remainder (~17pp central) reflects a combination of macro factor and noise, including retail margin expansion, demand-side substitution into similarly-tightening alternatives, and market expectations of further policy escalation.

Methodology: plausibility ranges, not statistical confidence intervals. The supply-share calculation: imports = ~60-65% of US fresh tomato consumption (USDA ERS); Mexico = ~90% of imports; therefore Mexico ≈ 57% of total US supply. Florida ≈ 12% of total US supply. Tariff range uses Mexico’s supply share × 17% duty × 70-100% pass-through. Climate ranges are sized to disclosed Florida disaster damage and Mexico mid-crop reporting (Mexico 2025 production -3% YoY per USDA FAS). Diesel and fertiliser sized to recent input-cost trajectory. The underlying series is BLS Average Price Data for field-grown fresh tomatoes (not the smoothed CPI tomato index). The directional argument — that climate and policy stack to produce the move, neither alone explains it — holds across the full range.

Did you enjoy this edition, if yes let me know and share it with someone who would benefit from our weekly insights.