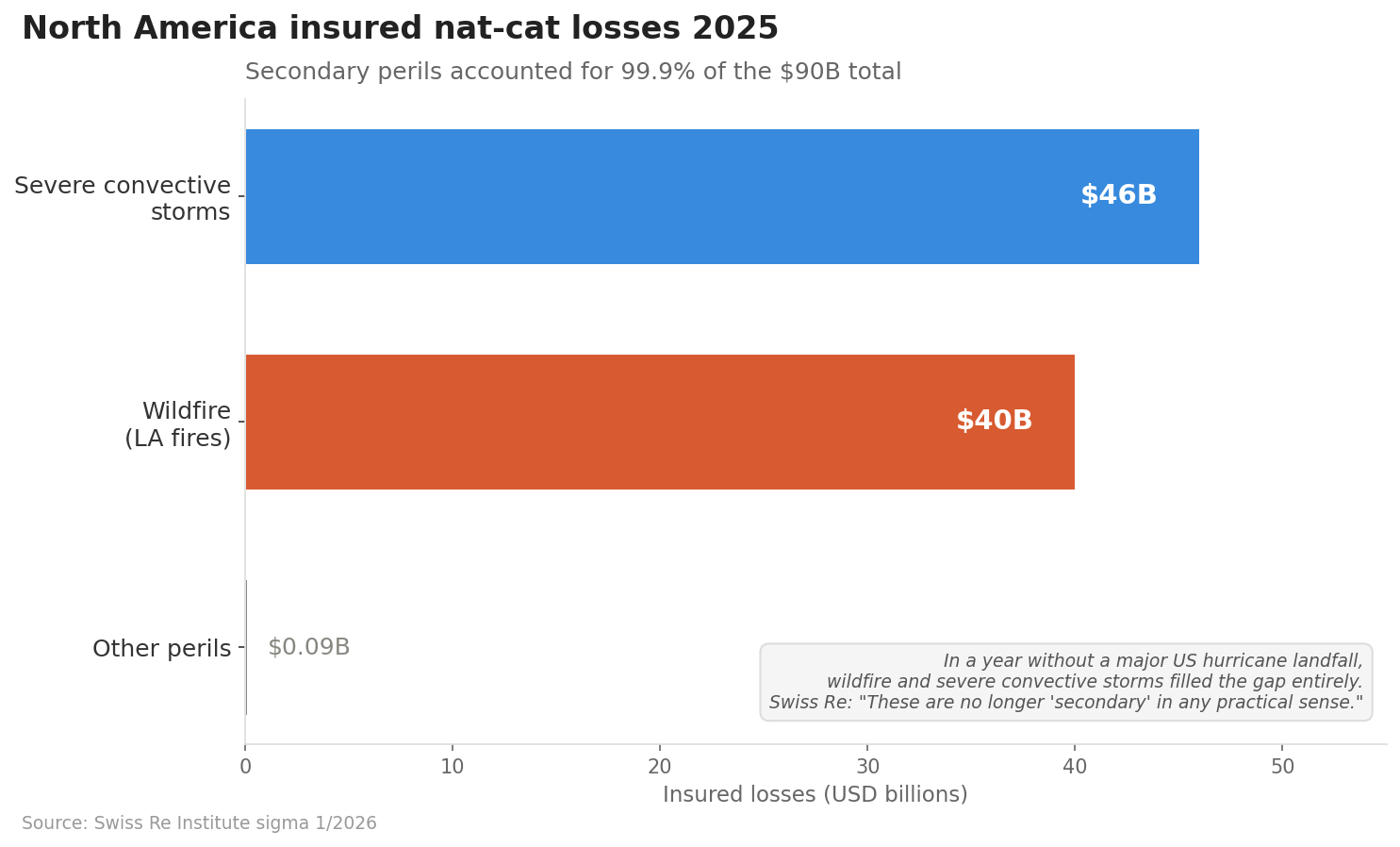

99.9%: When "Secondary" Becomes Primary

TL;DR

This week’s lead signal: Swiss Re’s latest sigma report shows secondary perils – wildfire and severe convective storms – accounted for 99.9% of North America’s $90 billion insured natural catastrophe losses in 2025. These perils are “no longer secondary in any practical sense.”

The implication: The insurance industry’s traditional hierarchy of peak vs. secondary perils no longer matches reality. Portfolio construction, capacity allocation, and pricing need to reflect a structurally higher baseline of losses from perils that behave like recurring operating costs, not tail events.

Lead Signal

Swiss Re: Secondary perils now dominate the loss landscape

Summary: Swiss Re Institute’s latest sigma report found that total insured losses surpassed $90 billion in 2025, below recent years but still reflecting a rising underlying risk trend. The striking finding: secondary perils accounted for almost the entire $90 billion in regional insured losses recorded in 2025. In a year without a major US hurricane landfall, wildfires and severe convective storms filled the gap entirely.

Key data: Wildfires and severe convective storms generated respectively about $40 billion and $46 billion in insured losses. Together, secondary perils made up 99.9% of 2025 insured nat-cat losses in the region.

Why this matters now: Swiss Re’s Monica Ningen put it plainly: “These are no longer ‘secondary’ in any practical sense.” She attributed the trend to exposure growth and underlying risk change, with more assets concentrated in the wildland-urban interface and weather patterns lifting both event frequency and severity.

The bigger point: For decades, catastrophe modelling and reinsurance capacity focused on “peak perils” – hurricanes and earthquakes. This report signals a structural shift. Even in a year without a major US hurricane landfall, insured losses remained elevated, pointing to a structurally higher baseline driven by more frequent high-impact events. The historical return period assumptions that underpin pricing, reserving, and capital allocation may no longer apply.

Read: Swiss Re sigma

This Week's Top Briefs

India: Heatwave intensifies as El Niño approaches

Summary: India is facing an intense and unusual heatwave this year, with temperatures already crossing 47°C in several regions. The India Meteorological Department (IMD) has signalled that ENSO-neutral conditions are evolving towards El Niño, with the World Meteorological Organization indicating El Niño could set in as early as May-July 2026.

Key data: Out of the 100 hottest cities globally, around 95 are in India. IMD forecasts monsoon rainfall at 92% of the long-period average..

Why it matters: India is a critical sourcing hub for textiles, pharmaceuticals, and agricultural commodities. Below-normal monsoons constrain rice and cotton production, stress hydropower generation, and compound heat-related labour productivity losses.

Read: Down to Earth, Medindia

US: Winter wheat conditions deteriorate as drought expands

Summary: USDA reports winter wheat at 35% good-to-excellent as drought impacts yields. The deterioration is sharpest in key Plains states, with soil moisture deficits pressuring crop development ahead of summer harvest.

Key data: As of April 5, 35% of winter wheat is rated good to excellent, down from 48% last year, while 31% is rated poor to very poor, a sharp increase from 21% in 2025. Oklahoma reports 54% of its crop in poor-to-very-poor condition, followed by Texas at 51% and Colorado at 49%.

Why it matters: Rainfall in the coming weeks will likely determine whether the winter wheat crop will be “made or broken for 2026.” The U.S. recorded its warmest and eighth-driest March in 132 years, accelerating evaporation and reducing irrigation reserves. Wheat futures rose 2.9% this week. A modest move, but one to watch if May rains fail to materialise.

Read: Fortune, USDA/Agrolatam

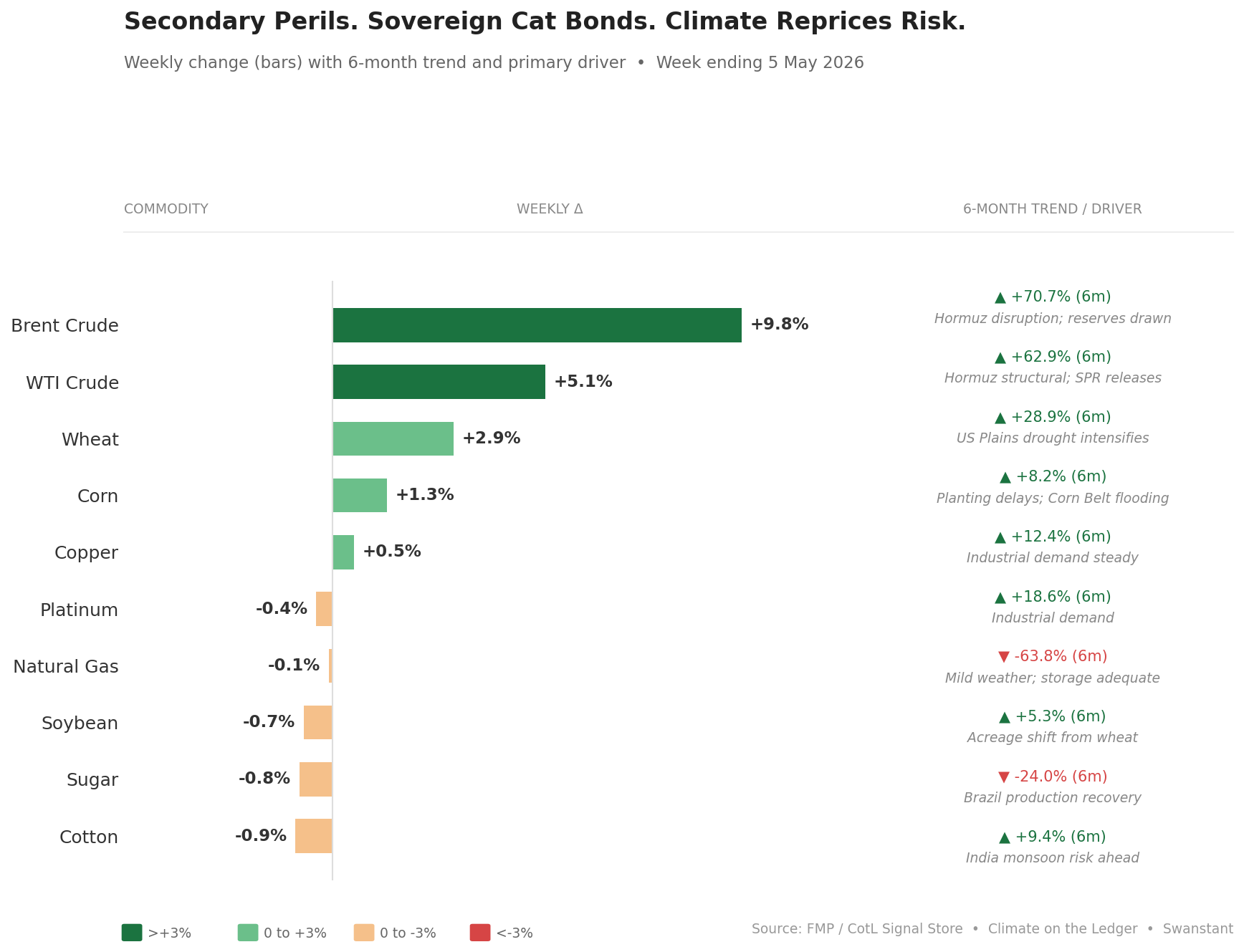

Cat bond market: Yields reach 9.3% as spreads widen ahead of hurricane season

Summary: Catastrophe bond market yields rose again through April 2026 to almost 9.3%. USAA, the most prolific cat bond sponsor, secured its largest issuance ever.

Key data: The overall yield coupon of the catastrophe bond market has risen another 2.3% to reach 9.27%. USAA has now successfully priced its largest catastrophe bond sponsorship ever at attractive spreads, with the Residential Reinsurance 2026 Limited cat bond providing $825 million in additional catastrophe reinsurance limit.

Why it matters: Seasonal spread widening reflects the market’s annual repricing of hurricane risk ahead of the June-November Atlantic season.

Read: Artemis, Artemis USAA

Adaptation Spotlight

ADB issues first sovereign cat bonds for Central Asia

Summary: The Asian Development Bank issued its first Disaster Relief Bond offerings as part of its regional Risk-Layered Disaster Relief Finance Program which aims to reduce the financial impact of natural hazards and climate-related shocks.

What they did: The two sovereign bonds – each $80 million in size and with a three-year tenor – will pay out to impacted communities if predefined levels of precipitation are breached, or if earthquakes reach particular magnitudes. The bonds leverage ADB’s AAA credit rating to transfer disaster risk from governments to private investors without exposing investors to sovereign credit risk.

Key outcome: “With this inaugural sovereign catastrophe bond, our developing member countries in Central Asia gain rapid, committed financing when disaster hits, so they can build back faster. This bond will pave the way for future issuances.” The precipitation trigger used is a “world-first catastrophe bond covering extreme precipitation risks.”

Why it matters: This is a template for how multilateral development banks can bridge the protection gap in vulnerable regions. The parametric structure – payouts triggered by predefined thresholds rather than damage assessments – ensures speed and transparency, critical for post-disaster recovery.

Read: ADB, Insurance Journal

Data Snapshot: Commodity & Freight Dashboard

Key Takeaways:

Crude surge continues. Brent +9.8% and WTI +5.1% as Strait of Hormuz continues to be at the center of oUS / Iran tensions.

Wheat +2.9% is the signal to watch. US Plains drought is biting: only 35% of winter wheat rated good-to-excellent (down from 48% last year). Oklahoma 54% poor-to-very-poor, Texas 51%. May rains will determine whether prices further escalade.

Forward risk: India monsoon. Cotton and rice prices are flat, but the developing El Niño and IMD’s below-normal monsoon forecast (92% of LPA) suggest supply risk for South Asian agricultural commodities in H2.

Methodology: Market prices on 5 May 2026 via FMP.

Did you enjoy this edition, if yes let me know and share it with someone who would benefit from our weekly insights.